![[The AI Show Episode 143]: ChatGPT Revenue Surge, New AGI Timelines, Amazon’s AI Agent, Claude for Education, Model Context Protocol & LLMs Pass the Turing Test](https://www.marketingaiinstitute.com/hubfs/ep%20143%20cover.png)

![Why modern UI is rarely written in C++? [closed]](https://cdn.sstatic.net/Sites/softwareengineering/Img/apple-touch-icon@2.png?v=1ef7363febba)

![From Accountant to Data Engineer with Alyson La [Podcast #168]](https://cdn.hashnode.com/res/hashnode/image/upload/v1744420903260/fae4b593-d653-41eb-b70b-031591aa2f35.png?#)

.png?#)

![Apple Posts Full First Episode of 'Your Friends & Neighbors' on YouTube [Video]](https://www.iclarified.com/images/news/96990/96990/96990-640.jpg)

![Apple May Implement Global iPhone Price Increases to Mitigate Tariff Impacts [Report]](https://www.iclarified.com/images/news/96987/96987/96987-640.jpg)

China-based SMS Phishing Triad Pivots to Banks

China-based purveyors of SMS phishing kits are enjoying remarkable success converting phished payment card data into mobile wallets from Apple and Google. Until recently, the so-called “Smishing Triad” mainly impersonated toll road operators and shipping companies. But experts say these groups are now directly targeting customers of international financial institutions, while dramatically expanding their cybercrime infrastructure and support staff.

China-based purveyors of SMS phishing kits are enjoying remarkable success converting phished payment card data into mobile wallets from Apple and Google. Until recently, the so-called “Smishing Triad” mainly impersonated toll road operators and shipping companies. But experts say these groups are now directly targeting customers of international financial institutions, while dramatically expanding their cybercrime infrastructure and support staff.

An image of an iPhone device farm shared on Telegram by one of the Smishing Triad members. Image: Prodaft.

If you own a mobile device, the chances are excellent that at some point in the past two years you’ve received at least one instant message that warns of a delinquent toll road fee, or a wayward package from the U.S. Postal Service (USPS). Those who click the promoted link are brought to a website that spoofs the USPS or a local toll road operator and asks for payment card information.

The site will then complain that the visitor’s bank needs to “verify” the transaction by sending a one-time code via SMS. In reality, the bank is sending that code to the mobile number on file for their customer because the fraudsters have just attempted to enroll that victim’s card details into a mobile wallet.

If the visitor supplies that one-time code, their payment card is then added to a new mobile wallet on an Apple or Google device that is physically controlled by the phishers. The phishing gangs typically load multiple stolen digital wallets onto a single Apple or Android device, and then sell those phones in bulk to scammers who use them for fraudulent e-commerce and tap-to-pay transactions.

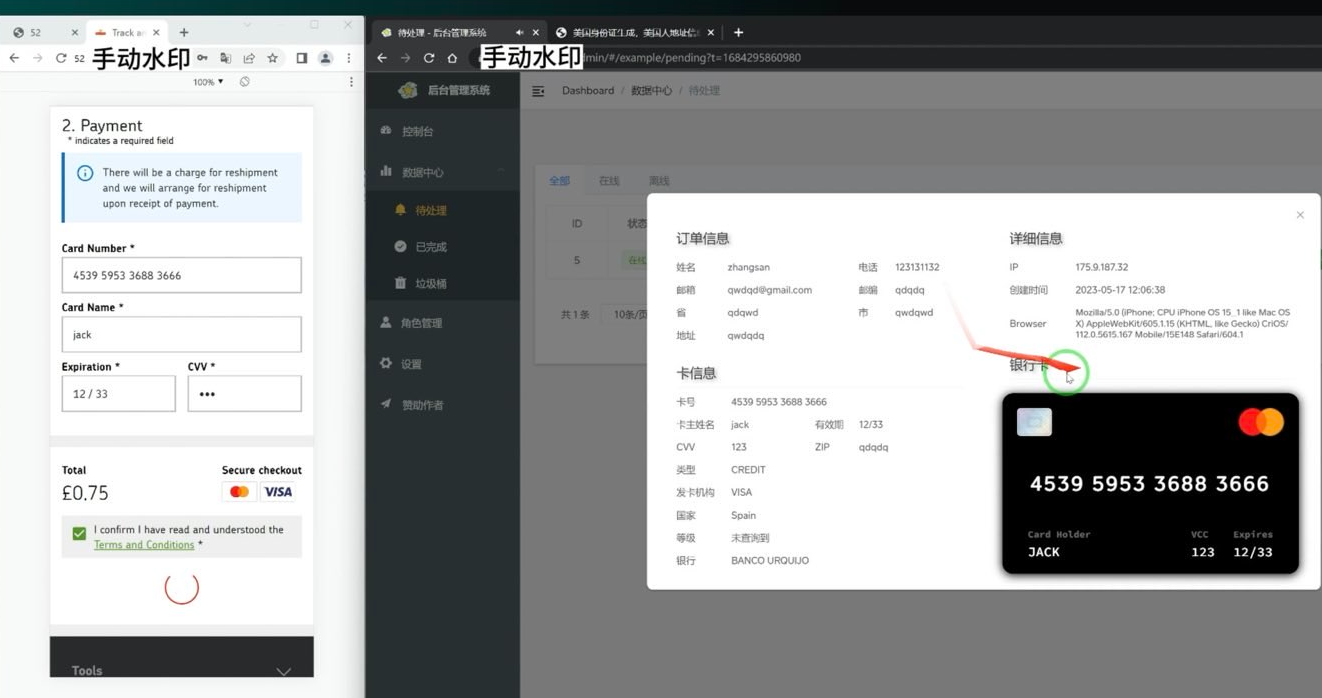

A screenshot of the administrative panel for a smishing kit. On the left is the (test) data entered at the phishing site. On the right we can see the phishing kit has superimposed the supplied card number onto an image of a payment card. When the phishing kit scans that created card image into Apple or Google Pay, it triggers the victim’s bank to send a one-time code. Image: Ford Merrill.

The moniker “Smishing Triad” comes from Resecurity, which was among the first to report in August 2023 on the emergence of three distinct mobile phishing groups based in China that appeared to share some infrastructure and innovative phishing techniques. But it is a bit of a misnomer because the phishing lures blasted out by these groups are not SMS or text messages in the conventional sense.

Rather, they are sent via iMessage to Apple device users, and via RCS on Google Android devices. Thus, the missives bypass the mobile phone networks entirely and enjoy near 100 percent delivery rate (at least until Apple and Google suspend the spammy accounts).

In a report published on March 24, the Swiss threat intelligence firm Prodaft detailed the rapid pace of innovation coming from the Smishing Triad, which it characterizes as a loosely federated group of Chinese phishing-as-a-service operators with names like Darcula, Lighthouse, and the Xinxin Group.

Prodaft said they’re seeing a significant shift in the underground economy, particularly among Chinese-speaking threat actors who have historically operated in the shadows compared to their Russian-speaking counterparts.

“Chinese-speaking actors are introducing innovative and cost-effective systems, enabling them to target larger user bases with sophisticated services,” Prodaft wrote. “Their approach marks a new era in underground business practices, emphasizing scalability and efficiency in cybercriminal operations.”

A new report from researchers at the security firm SilentPush finds the Smishing Triad members have expanded into selling mobile phishing kits targeting customers of global financial institutions like CitiGroup, MasterCard, PayPal, Stripe, and Visa, as well as banks in Canada, Latin America, Australia and the broader Asia-Pacific region.

Phishing lures from the Smishing Triad spoofing PayPal. Image: SilentPush.

SilentPush found the Smishing Triad now spoofs recognizable brands in a variety of industry verticals across at least 121 countries and a vast number of industries, including the postal, logistics, telecommunications, transportation, finance, retail and public sectors.

According to SilentPush, the domains used by the Smishing Triad are rotated frequently, with approximately 25,000 phishing domains active during any 8-day period and a majority of them sitting at two Chinese hosting companies: Tencent (AS132203) and Alibaba (AS45102).

“With nearly two-thirds of all countries in the world targeted by [the] Smishing Triad, it’s safe to say they are essentially targeting every country with modern infrastructure outside of Iran, North Korea, and Russia,” SilentPush wrote. “Our team has observed some potential targeting in Russia (such as domains that mentioned their country codes), but nothing definitive enough to indicate Russia is a persistent target. Interestingly, even though these are Chinese threat actors, we have seen instances of targeting aimed at Macau and Hong Kong, both special administrative regions of China.”

SilentPush’s Zach Edwards said his team found a vulnerability that exposed data from one of the Smishing Triad’s phishing pages, which revealed the number of visits each site received each day across thousands of phishing domains that were active at the time. Based on that data, SilentPush estimates those phishing pages received well more than a million visits within a 20-day time span.

The report notes the Smishing Triad boasts it has “300+ front desk staff worldwide” involved in one of their more popular phishing kits — Lighthouse — staff that is mainly used to support various aspects of the group’s fraud and cash-out schemes.

The Smishing Triad members maintain their own Chinese-language sales channels on Telegram, which frequently offer videos and photos of their staff hard at work. Some of those images include massive walls of phones used to send phishing messages, with human operators seated directly in front of them ready to receive any time-sensitive one-time codes.

As noted in February’s story How Phished Data Turns Into Apple and Google Wallets, one of those cash-out schemes involves an Android app called Z-NFC, which can relay a valid NFC transaction from one of these compromised digital wallets to anywhere in the world. For a $500 month subscription, the customer can wave their phone at any payment terminal that accepts Apple or Google pay, and the app will relay an NFC transaction over the Internet from a stolen wallet on a phone in China.

Chinese nationals were recently busted trying to use these NFC apps to buy high-end electronics in Singapore. And in the United States, authorities in California and Tennessee arrested Chinese nationals accused of using NFC apps to fraudulently purchase gift cards from retailers.

The Prodaft researchers said they were able to find a previously undocumented backend management panel for Lucid, a smishing-as-a-service operation tied to the XinXin Group. The panel included victim figures that suggest the smishing campaigns maintain an average success rate of approximately five percent, with some domains receiving over 500 visits per week.

“In one observed instance, a single phishing website captured 30 credit card records from 550 victim interactions over a 7-day period,” Prodaft wrote.

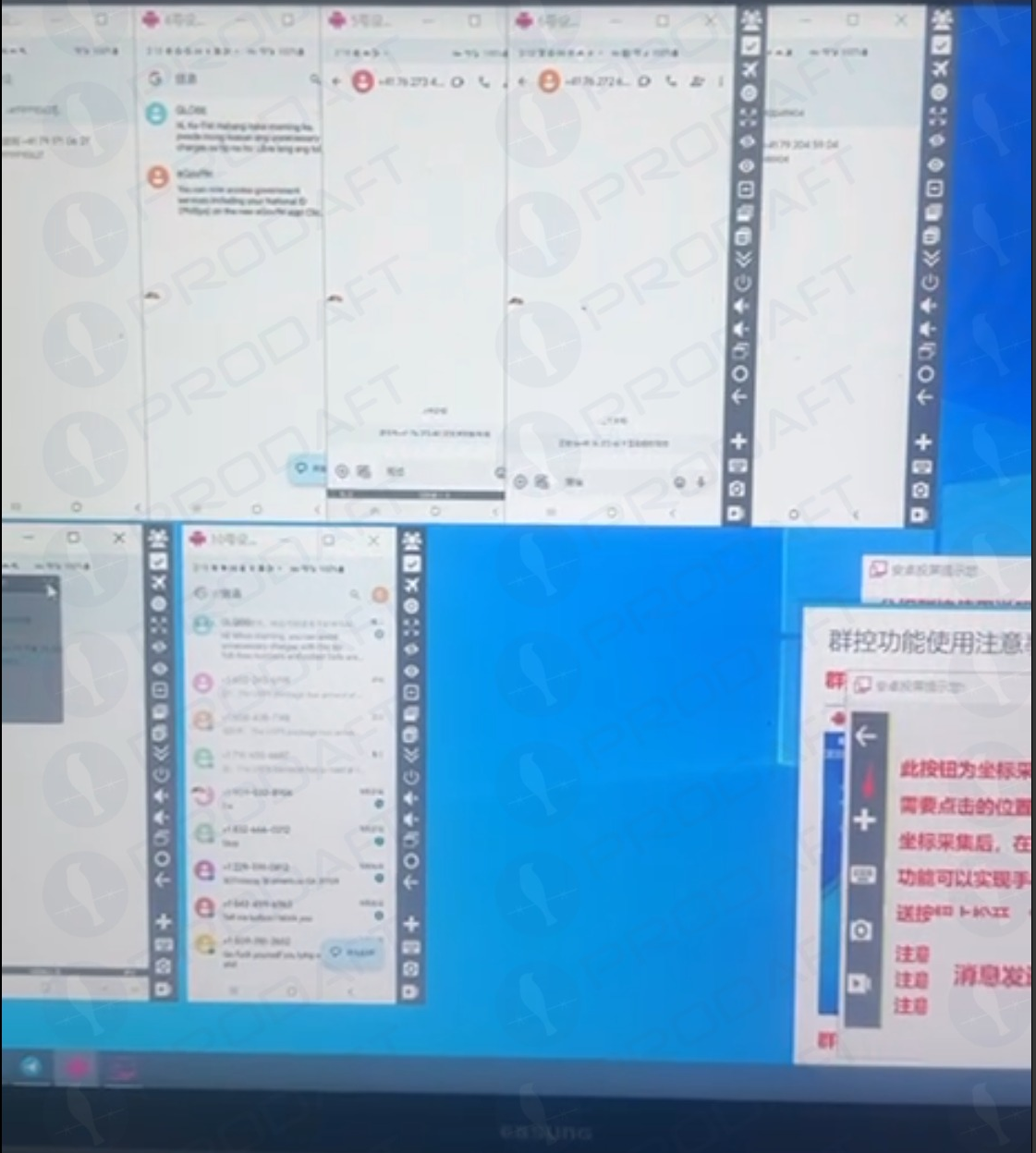

Prodaft’s report details how the Smishing Triad has achieved such success in sending their spam messages. For example, one phishing vendor appears to send out messages using dozens of Android device emulators running in parallel on a single machine.

Phishers using multiple virtualized Android devices to orchestrate and distribute RCS-based scam campaigns. Image: Prodaft.

According to Prodaft, the threat actors first acquire phone numbers through various means including data breaches, open-source intelligence, or purchased lists from underground markets. They then exploit technical gaps in sender ID validation within both messaging platforms.

“For iMessage, this involves creating temporary Apple IDs with impersonated display names, while RCS exploitation leverages carrier implementation inconsistencies in sender verification,” Prodaft wrote. “Message delivery occurs through automated platforms using VoIP numbers or compromised credentials, often deployed in precisely timed multi-wave campaigns to maximize effectiveness.

In addition, the phishing links embedded in these messages use time-limited single-use URLs that expire or redirect based on device fingerprinting to evade security analysis, they found.

“The economics strongly favor the attackers, as neither RCS nor iMessage messages incur per-message costs like traditional SMS, enabling high-volume campaigns at minimal operational expense,” Prodaft continued. “The overlap in templates, target pools, and tactics among these platforms underscores a unified threat landscape, with Chinese-speaking actors driving innovation in the underground economy. Their ability to scale operations globally and evasion techniques pose significant challenges to cybersecurity defenses.”

Ford Merrill works in security research at SecAlliance, a CSIS Security Group company. Merrill said he’s observed at least one video of a Windows binary that wraps a Chrome executable and can be used to load in target phone numbers and blast messages via RCS, iMessage, Amazon, Instagram, Facebook, and WhatsApp.

“The evidence we’ve observed suggests the ability for a single device to send approximately 100 messages per second,” Merrill said. “We also believe that there is capability to source country specific SIM cards in volume that allow them to register different online accounts that require validation with specific country codes, and even make those SIM cards available to the physical devices long-term so that services that rely on checks of the validity of the phone number or SIM card presence on a mobile network are thwarted.”

Experts say this fast-growing wave of card fraud persists because far too many financial institutions still default to sending one-time codes via SMS for validating card enrollment in mobile wallets from Apple or Google. KrebsOnSecurity interviewed multiple security executives at non-U.S. financial institutions who spoke on condition of anonymity because they were not authorized to speak to the press. Those banks have since done away with SMS-based one-time codes and are now requiring customers to log in to the bank’s mobile app before they can link their card to a digital wallet.