![[The AI Show Episode 150]: AI Answers: AI Roadmaps, Which Tools to Use, Making the Case for AI, Training, and Building GPTs](https://www.marketingaiinstitute.com/hubfs/ep%20150%20cover.png)

![[The AI Show Episode 149]: Google I/O, Claude 4, White Collar Jobs Automated in 5 Years, Jony Ive Joins OpenAI, and AI’s Impact on the Environment](https://www.marketingaiinstitute.com/hubfs/ep%20149%20cover.png)

![[PHP] Upgrading from PHP 7.4 to 8.1](https://media2.dev.to/dynamic/image/width%3D1000,height%3D500,fit%3Dcover,gravity%3Dauto,format%3Dauto/https:%2F%2Fdev-to-uploads.s3.amazonaws.com%2Fuploads%2Farticles%2Fqmaaabplfbcjejg2rr5n.png)

_ArtemisDiana_Alamy.jpg?width=1280&auto=webp&quality=80&disable=upscale#)

![In the market for a new router? Here are 13 models to avoid, according to the FBI [U]](https://i0.wp.com/9to5mac.com/wp-content/uploads/sites/6/2025/04/Most-Americans-are-paying-more-for-broadband-%E2%80%93-here-are-four-solutions.jpg?resize=1200%2C628&quality=82&strip=all&ssl=1)

![Galaxy S25 Ultra gets ‘Arc’ case that leaves the phone mostly exposed – available for Pixel 9 too [Gallery]](https://i0.wp.com/9to5google.com/wp-content/uploads/sites/4/2025/05/arc-pulse-case-galaxy-s25-ultra-1.jpg?resize=1200%2C628&quality=82&strip=all&ssl=1)

![Apple 15-inch M4 MacBook Air On Sale for $1023.86 [Lowest Price Ever]](https://www.iclarified.com/images/news/97468/97468/97468-640.jpg)

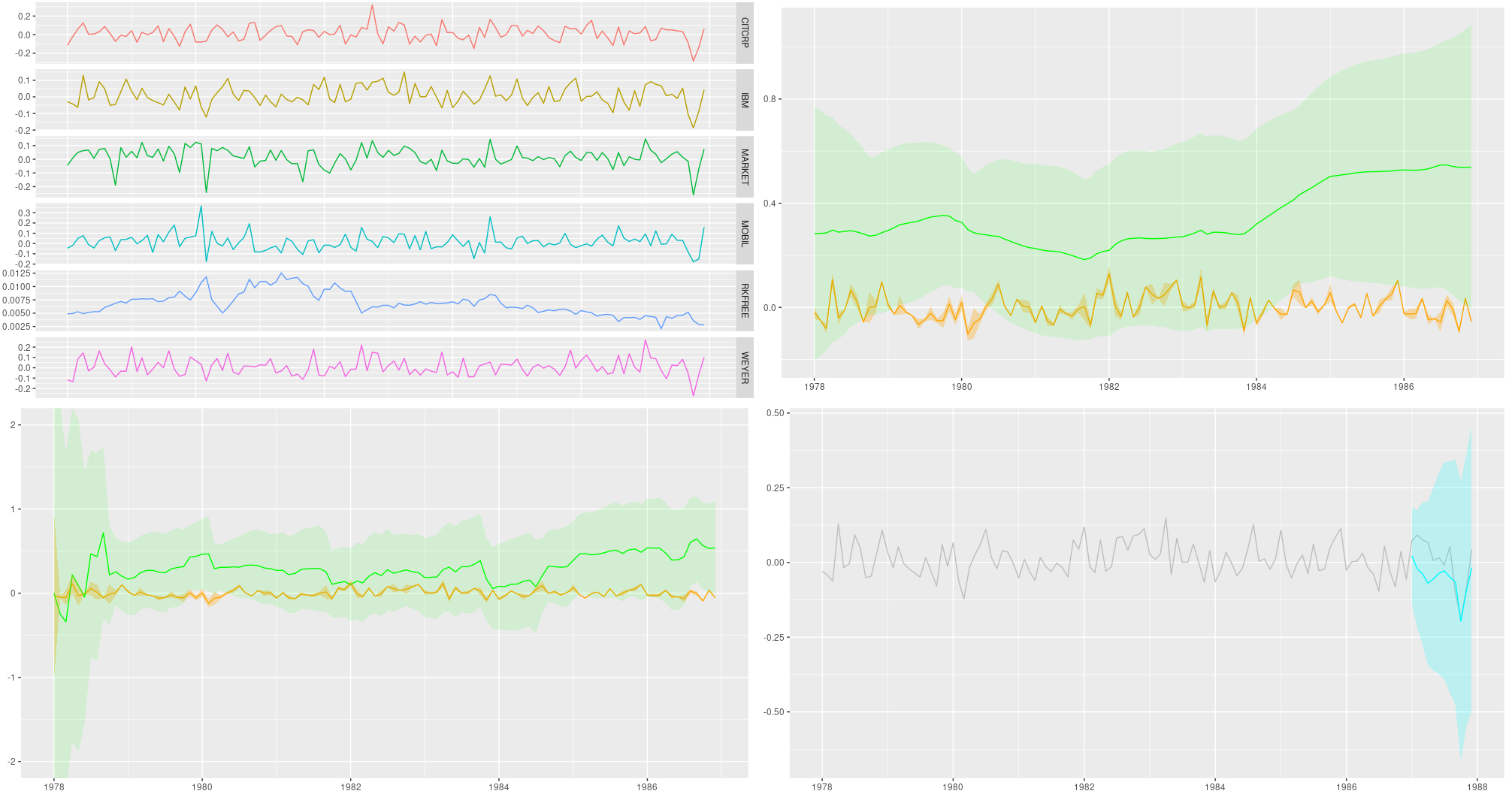

Dynamic linear models with tfprobability

Previous posts featuring tfprobability - the R interface to TensorFlow Probability - have focused on enhancements to deep neural networks (e.g., introducing Bayesian uncertainty estimates) and fitting hierarchical models with Hamiltonian Monte Carlo. This time, we show how to fit time series using dynamic linear models (DLMs), yielding posterior predictive forecasts as well as the smoothed and filtered estimates from the Kálmán filter.

Previous posts featuring tfprobability - the R interface to TensorFlow Probability - have focused on enhancements to deep neural networks (e.g., introducing Bayesian uncertainty estimates) and fitting hierarchical models with Hamiltonian Monte Carlo. This time, we show how to fit time series using dynamic linear models (DLMs), yielding posterior predictive forecasts as well as the smoothed and filtered estimates from the Kálmán filter.