![[Free Webinar] Guide to Securing Your Entire Identity Lifecycle Against AI-Powered Threats](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEjqbZf4bsDp6ei3fmQ8swm7GB5XoRrhZSFE7ZNhRLFO49KlmdgpIDCZWMSv7rydpEShIrNb9crnH5p6mFZbURzO5HC9I4RlzJazBBw5aHOTmI38sqiZIWPldRqut4bTgegipjOk5VgktVOwCKF_ncLeBX-pMTO_GMVMfbzZbf8eAj21V04y_NiOaSApGkM/s1600/webinar-play.jpg?#)

![[The AI Show Episode 145]: OpenAI Releases o3 and o4-mini, AI Is Causing “Quiet Layoffs,” Executive Order on Youth AI Education & GPT-4o’s Controversial Update](https://www.marketingaiinstitute.com/hubfs/ep%20145%20cover.png)

_Jochen_Tack_Alamy.png?width=1280&auto=webp&quality=80&disable=upscale#)

-xl.jpg)

![New Hands-On iPhone 17 Dummy Video Shows Off Ultra-Thin Air Model, Updated Pro Designs [Video]](https://www.iclarified.com/images/news/97171/97171/97171-640.jpg)

![Apple Shares Trailer for First Immersive Feature Film 'Bono: Stories of Surrender' [Video]](https://www.iclarified.com/images/news/97168/97168/97168-640.jpg)

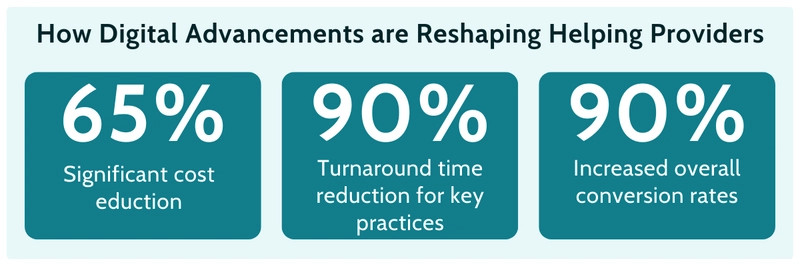

Accelerating Insurance Digital Transformation: 2025 Outlook

Understanding Digital Transformation in the Insurance Industry These days digital transformation in insurance goes far beyond moving paper forms to PDFs or launching a customer portal. That sort of initiative could have been considered innovative ten years ago, but in 2025, insurers need to move further. The Drivers of Change in the Insurance Sector Transformation in insurance is driven by several converging forces. Traditional operating models are reaching their limits, with legacy systems proving costly, inflexible, and a barrier to innovation. At the same time, evolving regulations demand greater transparency, real-time reporting, and advanced risk modeling—needs that require modern digital infrastructures. Competition from insurtechs and digital-native startups is also raising customer expectations for seamless, flexible experiences. Internally, forward-looking executives recognize that digital transformation is no longer just about efficiency, but rather it’s essential for growth, resilience, and competitive differentiation. The Demand for Digital Solutions is Growing Insurance companies are actively seeking solutions that allow them to innovate faster and serve customers better. This is particularly true in segments that rely on complex or highly specialized products—where agility and configurability are key. Here a clear shift toward digitalization is underway: 89% of companies have already adopted or plan to adopt a digital-first business strategy. Looking ahead, 74% of insurance executives worldwide have identified digital transformation and technology adoption as their top strategic priorities — ranking it above other major concerns like ESG initiatives and talent acquisition. Customers are Looking for Digital Channels But the main reason for the push towards digital transformation and why insurers need to take it seriously is changing consumer behaviors. People now expect the same level of digital convenience from their insurer as they get from their bank or their favorite e-commerce platform. This means modern mobile apps, self-service portals, real-time **policy management **and updates, and fast, transparent claims handling. Five Dimensions of Successful Digital Transformation In which sectors and areas of their internal operations should insurers invest to achieve the best return on their digital transformation efforts? There are five general dimensions to consider, but which should be prioritized depends on each insurer’s specific situation. The key takeaway is that these dimensions rarely operate in isolation. In most cases, all areas require attention and investment to ensure a successful transformation. Modernizing Legacy Insurance Software Infrastructure First, we need to address legacy insurance software. Most established insurers still rely heavily on legacy core systems – rigid, monolithic platforms that are deeply embedded in underwriting, claims, and policy administration processes. From our experience, we noticed that this problem is much more common than many people might suspect. While these systems are stable, they weren’t designed for the speed and flexibility that today’s marketplace demands. Insurance software modernization doesn’t have to mean ripping everything out. An incremental approach-such as building API layers around core systems, gradually decoupling services, or leveraging middleware-allows insurers to innovate on top of existing infrastructure without risking operational disruption. Building a Modern Data Infrastructure to Support Real-Time Decisions Data is the backbone of digital transformation—but only if it’s accurate, accessible, and actionable. A key enabler here is multitenancy—especially in platforms serving multiple insurance lines or partner programs. A multitenant architecture allows insurance professionals to manage separate data environments for each entity or client while maintaining centralized control and scalability. Combined with streaming data pipelines, AI-ready analytics engines, and strict data governance models, this approach supports both agility and compliance. Cloud vs On-Premise: Choosing the Right Model for Long-Term Flexibility While cloud infrastructure offers clear advantages—faster deployments, seamless scalability, and reduced maintenance—it’s not always the default answer in insurance. In certain regulated markets, especially where data sovereignty or auditability is a concern, on-premise deployment is still a legal or practical requirement. In addition, the economics of the cloud must be carefully considered. As cloud costs continue to rise and usage scales, exuberant pricing models can begin to undermine the long-term ROI of cloud-native solutions. For insurers with predictable workloads and in-house IT capacity, on-premises or hybrid models can provide greater cost control and regulatory clarity. Unlocki

Understanding Digital Transformation in the Insurance Industry

These days digital transformation in insurance goes far beyond moving paper forms to PDFs or launching a customer portal.

That sort of initiative could have been considered innovative ten years ago, but in 2025, insurers need to move further.

The Drivers of Change in the Insurance Sector

Transformation in insurance is driven by several converging forces.

Traditional operating models are reaching their limits, with legacy systems proving costly, inflexible, and a barrier to innovation.

At the same time, evolving regulations demand greater transparency, real-time reporting, and advanced risk modeling—needs that require modern digital infrastructures.

Competition from insurtechs and digital-native startups is also raising customer expectations for seamless, flexible experiences.

Internally, forward-looking executives recognize that digital transformation is no longer just about efficiency, but rather it’s essential for growth, resilience, and competitive differentiation.

The Demand for Digital Solutions is Growing

Insurance companies are actively seeking solutions that allow them to innovate faster and serve customers better.

This is particularly true in segments that rely on complex or highly specialized products—where agility and configurability are key. Here a clear shift toward digitalization is underway: 89% of companies have already adopted or plan to adopt a digital-first business strategy.

Looking ahead, 74% of insurance executives worldwide have identified digital transformation and technology adoption as their top strategic priorities — ranking it above other major concerns like ESG initiatives and talent acquisition.

Customers are Looking for Digital Channels

But the main reason for the push towards digital transformation and why insurers need to take it seriously is changing consumer behaviors.

People now expect the same level of digital convenience from their insurer as they get from their bank or their favorite e-commerce platform.

This means modern mobile apps, self-service portals, real-time **policy management **and updates, and fast, transparent claims handling.

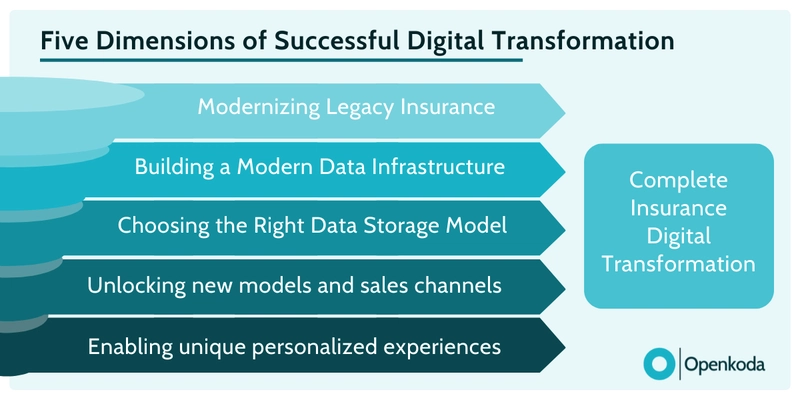

Five Dimensions of Successful Digital Transformation

In which sectors and areas of their internal operations should insurers invest to achieve the best return on their digital transformation efforts?

There are five general dimensions to consider, but which should be prioritized depends on each insurer’s specific situation.

The key takeaway is that these dimensions rarely operate in isolation. In most cases, all areas require attention and investment to ensure a successful transformation.

Modernizing Legacy Insurance Software Infrastructure

First, we need to address legacy insurance software.

Most established insurers still rely heavily on legacy core systems – rigid, monolithic platforms that are deeply embedded in underwriting, claims, and policy administration processes. From our experience, we noticed that this problem is much more common than many people might suspect.

While these systems are stable, they weren’t designed for the speed and flexibility that today’s marketplace demands.

Insurance software modernization doesn’t have to mean ripping everything out.

An incremental approach-such as building API layers around core systems, gradually decoupling services, or leveraging middleware-allows insurers to innovate on top of existing infrastructure without risking operational disruption.

Building a Modern Data Infrastructure to Support Real-Time Decisions

Data is the backbone of digital transformation—but only if it’s accurate, accessible, and actionable.

A key enabler here is multitenancy—especially in platforms serving multiple insurance lines or partner programs.

A multitenant architecture allows insurance professionals to manage separate data environments for each entity or client while maintaining centralized control and scalability. Combined with streaming data pipelines, AI-ready analytics engines, and strict data governance models, this approach supports both agility and compliance.

Cloud vs On-Premise: Choosing the Right Model for Long-Term Flexibility

While cloud infrastructure offers clear advantages—faster deployments, seamless scalability, and reduced maintenance—it’s not always the default answer in insurance. In certain regulated markets, especially where data sovereignty or auditability is a concern, on-premise deployment is still a legal or practical requirement.

In addition, the economics of the cloud must be carefully considered. As cloud costs continue to rise and usage scales, exuberant pricing models can begin to undermine the long-term ROI of cloud-native solutions.

For insurers with predictable workloads and in-house IT capacity, on-premises or hybrid models can provide greater cost control and regulatory clarity.

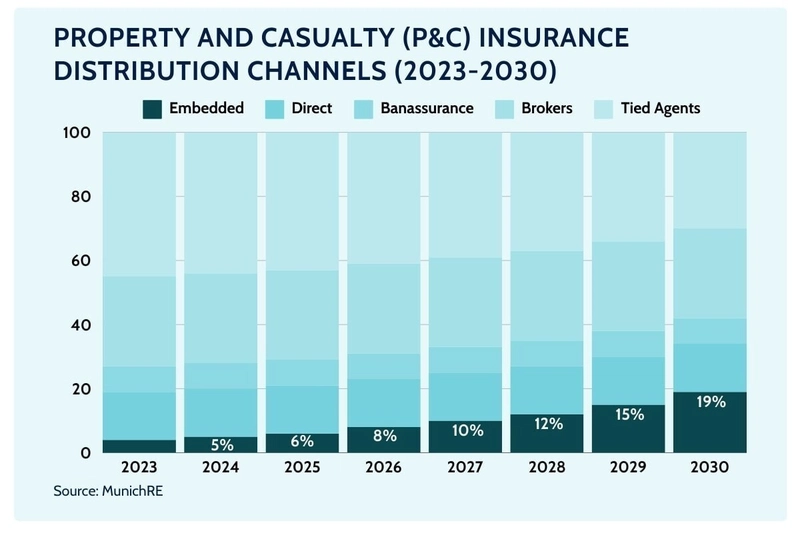

Unlocking new business models and sales channels

With the right tech stack, insurers can tap into emerging opportunities such as embedded insurance, usage-based products, digital affinity programs, and dynamic bundling.

These models allow insurance to be sold as a service, integrated into everyday transactions and platforms—from booking engines to subscription services.

Achieving this, however, requires a flexible application core—one that can easily adapt to different product configurations, APIs, and front-end experiences. Insurers with composable systems are able to experiment, partner, and pivot quickly, unlocking distribution channels that would be out of reach with a rigid, traditional platform.

Personalizing experiences

Last but not least, there’s the aspect of improving personalization.

The key thing to remember here is that true personalization goes beyond marketing automation – the thing most people associate with that ever-popular term.

True personalization should touch pricing models, product design, and real-time engagement – the more, the better.

For insurers, this means having the right data flows, decision engines, and feedback loops in place. A digitally transformed organization can deliver contextual, meaningful experiences while gathering the insights needed to constantly refine them.

Case Studies and Real-World Examples

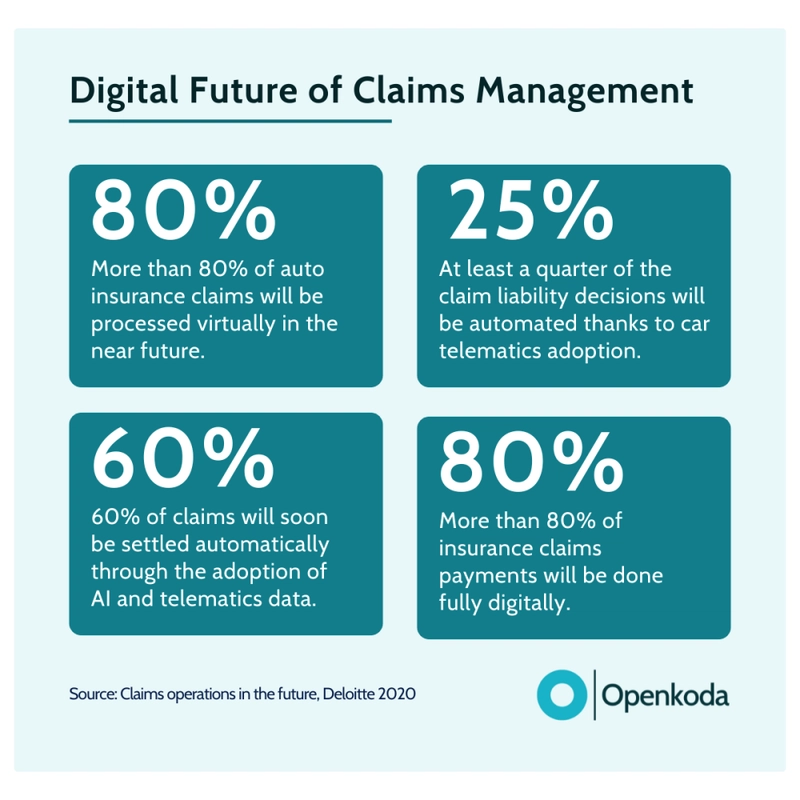

Building Custom Claims Management Software in Minutes with Rapid Software Development Platform

One of the most resource-intensive areas of insurance operations is claims management.

From initial submission to validation and resolution, the claims process often involves multiple departments, disparate systems, and significant manual intervention.

This process can be particularly challenging for insurers operating in niche markets, where out-of-the-box solutions are often unable to handle complex data types and processes.

In these cases, a bespoke approach is the only viable option.

Typically, this process takes months of meticulous planning, development, and testing and costs tens or even hundreds of thousands of dollars, but what if there was a way to speed up this process by up to 60% and have a working prototype in minutes?

It seems impossible, but with Insurtech development platforms like Openkoda, it’s entirely possible.

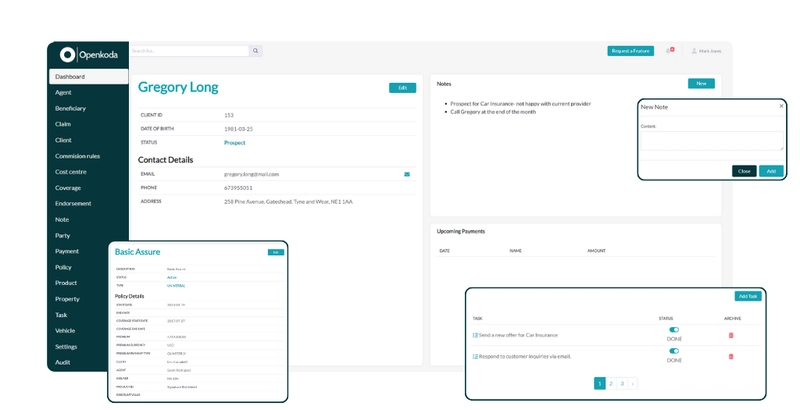

Openkoda enables fast, intuitive setup of claims data models—claim numbers, statuses, descriptions, and policy references can be configured in just a few clicks. No large engineering team required.

Want a custom dashboard that shows key metrics and recent claim statuses at a glance for improved data analytics? You’ve got it. Need custom reminders so that your team can stay up to date with policy statuses? A couple of clicks, and it’s live.

As claims volumes increase or your workflows grow more complex, you can easily:

- Automate repetitive tasks using custom logic and workflow triggers

- Assign role-based permissions to protect sensitive data and support regulatory compliance

- Integrate with external tools (payment providers, policy systems, fraud detection engines) via open APIs

- Attach supporting documents to claim records, ensuring everything is in one place

- Export and import large datasets as needed for analysis or migration

The result? A fully functional MVP of a claims management app, ready to adapt and grow with your business.

[Read also: How to Automate Insurance Policy Renewal Reminders?]

Creating Embeddedable Insurance Forms for Auto Insurance Company

Car insurance is a natural fit for embedded distribution.

Think about the customer journey: someone buying a car online, visiting a dealership website, or even browsing financing options is already primed to consider coverage.

Offering a tailored quote right there, as part of that journey, eliminates friction — and dramatically increases the likelihood of conversion.

Here’s how easy it is to go from idea to working prototype:

- Step #1: Build a Smart Quote Form: Use Openkoda’s built-in tools to create a responsive form that collects all the necessary info — vehicle registration, model, insurance type, and more. You can design the fields to adapt based on the user’s input, keeping things simple and relevant.

- Step #2: Configure Real-Time Pricing Logic: Add business logic that dynamically calculates the premium. This can be as straightforward or as advanced as you need — from flat rates to formulas pulling in external risk data or discount schemes.

- Step #3: Embed Anywhere: Once ready, the form can be dropped directly into any website or partner platform. Whether it’s a dealership site, car loan portal, or automotive app, the integration is seamless and user-friendly.

- Step #4: Customize, Extend, Repeat: As with all Openkoda components, everything is fully customizable. If you need new API integrations with underwriting engines or multi-language support you can do it easily and efficiently thanks to the extensible core.

Implementing a Dynamic Pricing & Real-Time Premium Calculation in Insurance Systems

Launching an innovative insurance product is rarely a one-and-done effort.

From the pilot phase to post-launch, insurers are constantly tweaking: pricing formulas, discount rules, eligibility criteria, and more.

Maybe you’re responding to market feedback, optimizing for profitability, or adapting to partner requirements.

Static systems just don’t cut it anymore.

With Openkoda, implementing dynamic pricing is much faster — even for non-technical users.

The platform lets you build custom pricing logic using straightforward, readable code snippets that can be updated, tested, and deployed on the go.

Here’s what that looks like in practice:

- Custom Pricing Logic Create and manage pricing rules in a dedicated logic editor. Whether you need to calculate premiums based on age, location, car type, or claims history, you can define it all in a clear and transparent way.

- Business-Friendly Editing Need to adjust the formula for a specific campaign or launch a time-based discount? You don’t have to redeploy the app. Just update the rule and it goes live instantly.

- Scenario Testing and Experimentation Want to try out multiple pricing strategies to see what converts best? Openkoda allows you to run A/B tests or region-specific pricing variations without any major restructuring.

- Integrate External Data Sources Pull in real-time data like weather, traffic, or credit scores to influence pricing dynamically — giving you even more control over risk and profitability.

In short: if you’re building or scaling modern insurance products, dynamic pricing becomes essential.

And with Openkoda, you get that flexibility without sacrificing control, security, or speed.

.

Digital Transformation in Insurance Industry: Closing Thoughts

Digital transformation is no longer optional—it’s the foundation for future-ready insurance organizations.

As technology reshapes customer expectations, product delivery, and operational models, insurers must move from incremental improvements to holistic reinvention.

Those who act decisively today will define the market standards of tomorrow